The short version.

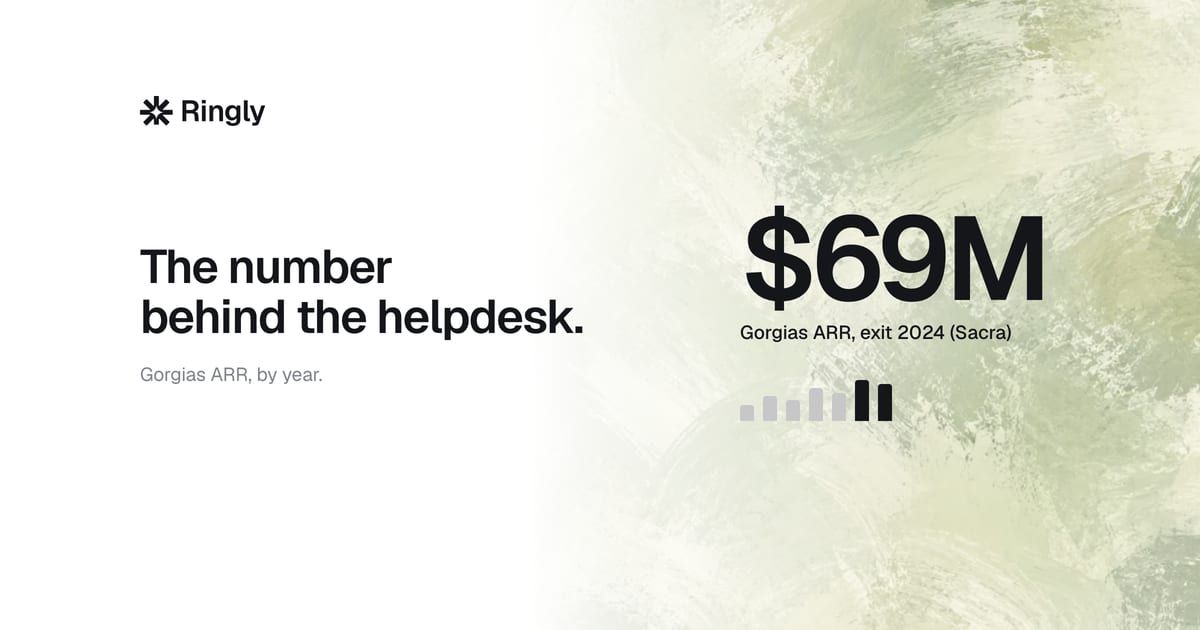

- The number: Gorgias exited 2024 at roughly $69M in ARR (Sacra). No official 2025 figure is public yet. At its 30%-plus growth rate, that tracks toward the high-$70Ms to around $85-90M run-rate through 2025.

- The shape: $25M ARR in 2022, $51M in 2023, $69M in 2024. A $530M valuation off the May 2024 Series C, 15,000-plus merchants, around 475 employees.

- If you run a $10M-$100M Shopify brand on Gorgias: the ARR tells you they're winning at chat and email. It doesn't tell you your phone queue is covered. That's the gap worth watching.

Gorgias's ARR was roughly $69M exiting 2024, according to Sacra, and the company has not published an official 2025 figure. At the 34% year-over-year growth it posted from 2023 to 2024, a reasonable directional estimate puts Gorgias somewhere in the high-$70Ms to around $85-90M run-rate through 2025. That's the answer if you came here for the number. If you run customer experience at a Shopify brand doing $10M-$100M, you probably didn't come here as an investor. You came because you already pay Gorgias, and a vendor's ARR is the quickest proxy for "are they going to be around, and are they winning."

So this post does both. It gives you the sourced number and the trajectory, and then it gives you the part the financial profiles skip: what a healthy Gorgias ARR actually means for your stack, and the one channel that growth doesn't fix.

I'm Ruben, co-founder of Ringly. We run AI phone support for 50-plus Shopify brands, and a lot of them run Gorgias next to us. So I look at Gorgias's numbers the way a buyer does, not an analyst. If you want to skip the reading and just see where your own missed calls are leaking, book a 30-min call and we'll pull the last 7 days live.

Gorgias ARR by year (the short answer)

Here's the trajectory, pulled from the most-cited public estimates. Gorgias roughly doubled ARR from 2022 to 2023, then added another 34% into 2024, which is the kind of curve that keeps investors interested and competitors nervous.

| Year | ARR (Sacra) | YoY growth | Note |

|---|---|---|---|

| 2022 | $25M | n/a | Sacra estimate |

| 2023 | $51M | ~100% | Sacra estimate |

| 2024 | $69M | 34% | Sacra, exit ARR |

| 2025 | not officially disclosed | est. 30%+ | directional: high-$70Ms to ~$85-90M |

One thing worth flagging up front. There are two main public estimates and they don't perfectly agree. Sacra puts 2024 ARR at $69M. Getlatka puts 2024 revenue at $72.6M. That's a gap of about $3.6M, and it's not a contradiction anyone's hiding. It's two firms using different models to estimate a private company that doesn't open its books. I lean on Sacra here because it's the more frequently updated and more widely cited of the two, but both land in the same neighborhood: high-$60Ms to low-$70Ms exiting 2024.

Why there's no official 2025 ARR number

Gorgias is private. Private companies disclose revenue when it helps them (a funding round, a press milestone) and stay quiet otherwise. There's no 10-K, no earnings call, no obligation to confirm a number.

The honest read for 2025: nobody outside Gorgias has the exact figure, and anyone publishing a precise 2025 ARR is estimating. What we can say with confidence is the direction. If Gorgias held even a softened version of its 30%-plus growth, exiting-2024's $69M compounds to somewhere in the mid-$80Ms to $90M run-rate by the end of 2025. Treat that as an estimate, not a disclosure.

If you need a number you can defend in a board deck, cite "$69M ARR (2024, Sacra)" and note that 2025 is unconfirmed. That's the defensible position. The reason this matters for an operator is simple: you're using ARR as a confidence signal, and the confidence signal is strong either way. Gorgias is not a shrinking vendor.

Worth saying plainly, because most of the SERP won't: anyone publishing a precise "Gorgias ARR 2025: $X" headline is reverse-engineering it from headcount, app-store reviews, and the last disclosed round. That's a reasonable estimate. It is not a fact. The number you can stand behind is the 2024 one.

Gorgias valuation and funding

Gorgias was valued at $530M in its May 2024 Series C, which worked out to roughly an 8.8x forward revenue multiple at the ~$60M ARR it was running mid-year, per Sacra's research note. For a vertical SaaS company growing 30%-plus, that multiple is healthy without being frothy.

| Metric | Figure | Source |

|---|---|---|

| Valuation | $530M (May 2024 Series C) | Sacra |

| Forward revenue multiple | ~8.8x | Sacra |

| Total funding raised | ~$104M across 9 rounds | Sacra |

| Notable investors | Shopify, Sapphire Ventures, Flex Capital | Sacra |

The Shopify investment is the one to notice. Shopify doesn't put money into many of its app-store vendors, and Gorgias is its only Premier Partner for CX. That relationship is part of why Gorgias sits so deep in the top-merchant tier, which we'll get to next.

How big is Gorgias, really

Numbers on a funding page don't tell you whether a vendor is embedded or just well-funded. Here's the scale that actually matters for an operator.

- Merchants: 15,000-plus ecommerce brands worldwide, per Sacra and corroborated in our own breakdown of Gorgias's customer count.

- Top-tier concentration: roughly 40% of Shopify's top 1,500 merchants run Gorgias. The strength is among bigger, higher-volume brands, not the long tail of small stores.

- Headcount: around 475 employees (Getlatka reported 476 as of December 2024, up from 332 a year earlier).

- Founded: 2015, by Romain Lapeyre and Alex Plugaru, headquartered in San Francisco.

Gorgias is the top-rated customer service app on the Shopify App Store, and its average contract value sits around $12.1K, per Getlatka, which tells you the customer base skews toward serious brands rather than hobby stores. If you're a $10M-$100M operator, that's your peer set. The product was built for you, the same way our own Shopify-Plus customer-service playbook is.

The headcount jump is its own signal. Going from roughly 332 employees to 476 in a single year is a company hiring against growth, not trimming to survive it. For a vendor you're trusting with your support stack, that's the read you want. It also explains the ARR curve: more people building, more product surface, more reasons for an existing customer to spend more next year than they did last year.

The growth story is an AI-monetization story

Here's the part the ARR ladder hides. Gorgias didn't just add customers to get from $51M to $69M. It re-priced around AI.

Gorgias charges by ticket and resolution, not by seat. Its AI Agent runs around $0.90 per resolution on annual billing (closer to $1.00 monthly), and overage above your bundled allotment jumps to $1.50 per resolution. That's a 67% step up at the margin. The same lever that compounds Gorgias's ARR is the lever that moves your bill at volume.

That's the trade you're making: a consumption-priced AI helpdesk means the vendor grows when your volume grows, and so does your invoice. It's not a knock. It's just the mechanic, and it's worth understanding before you deepen the dependency. One more honest note from the field: Gorgias markets up to 60% automation, but published case studies tend to land in the 26-56% range. Plan your budget against the lower end, not the marketing number.

If you want the full picture on what you'll actually pay, our Gorgias pricing breakdown walks the tiers and the AI agent line item.

What Gorgias's ARR means for your stack

So Gorgias is winning. The ARR is healthy, the growth is real, the Shopify relationship is deep. If you're using the number as a "should I trust this vendor long-term" signal, the answer is yes for chat and email. Gorgias is a strong helpdesk, and a $69M ARR vendor isn't going anywhere.

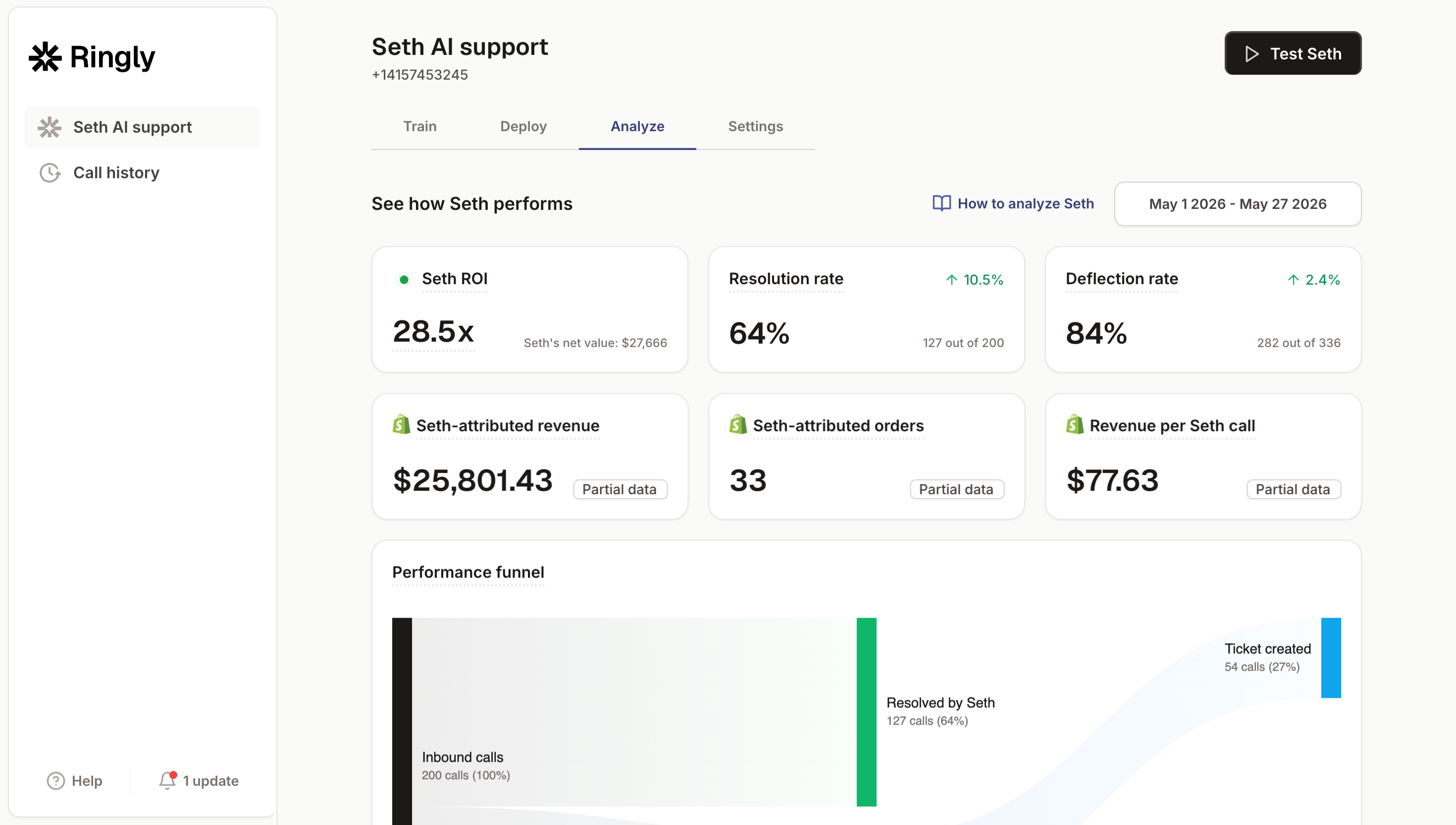

But here's what the ARR doesn't tell you. None of that growth fixed your phone queue. When we pull the last 7 days of missed calls for a brand that already runs Gorgias, the phone is the one channel all that ARR growth never touched. Tickets get handled. The voicemails nobody returns, the after-hours calls, the WISMO calls that ring while your reps are asleep, those still leak. WISMO alone is 30-40% of support contacts and over 50% at peak, per Salesforce, and a real share of it comes in by phone at $250-plus AOV brands.

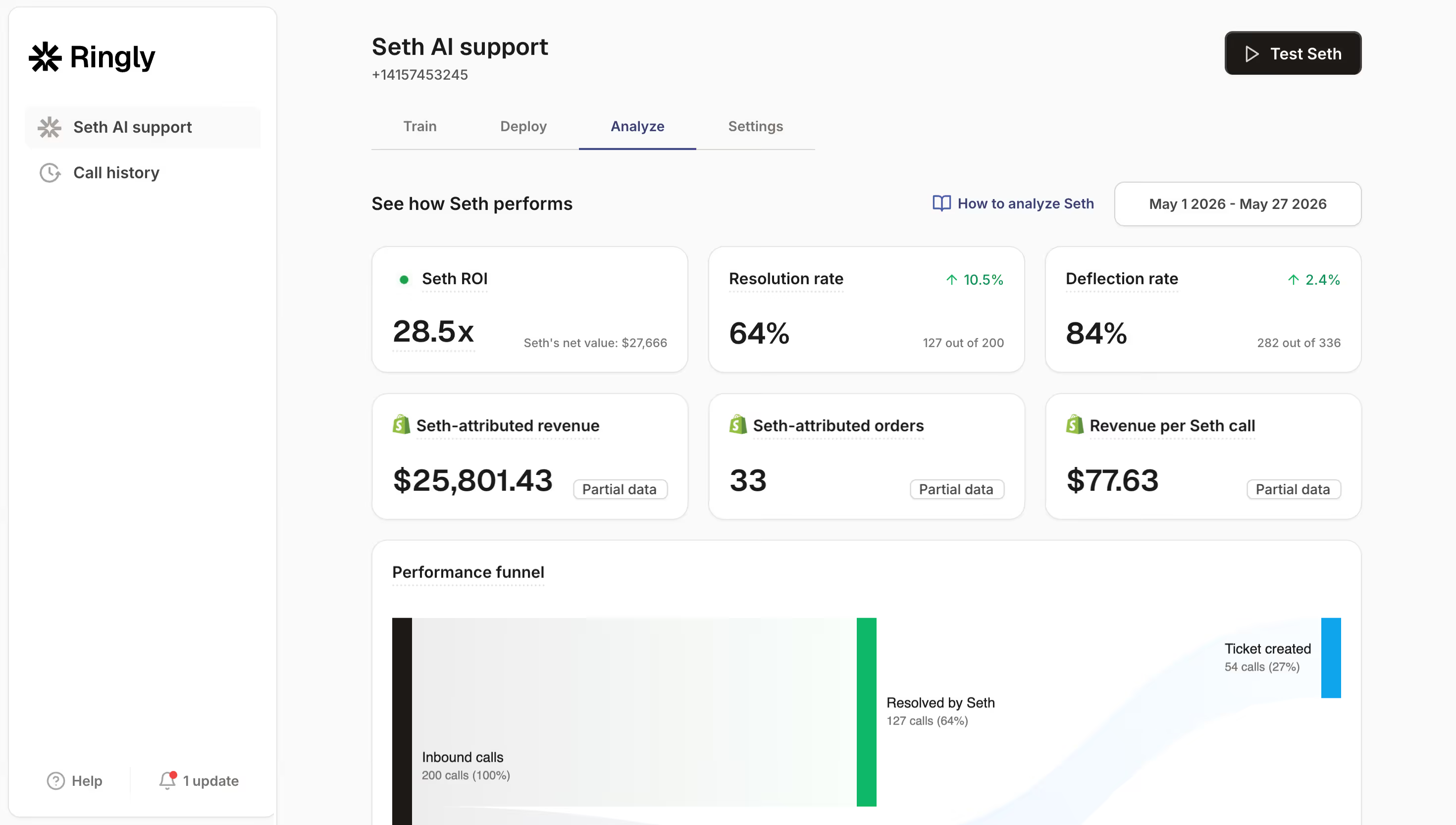

That's the channel we run. Ringly is AI phone support for Shopify brands that sits in front of your helpdesk, not instead of it. Across 50-plus brands, the AI resolves 73% of inbound calls on its own at roughly $0.42 per resolved call, and anything that needs a person escalates cleanly into Gorgias. WashCo, a Shopify brand we launched, recovered $22,664 in its first 7 days on the phone.

The math is the same shape as your helpdesk math, just on the channel Gorgias doesn't lead.

| Line item | Today | With Ringly |

|---|---|---|

| 6 reps × $4K loaded | $24,000/mo | n/a |

| Ringly (~$5K/mo) | n/a | $5,000/mo |

| Net monthly CS spend | $24,000/mo | $5,000/mo |

| Monthly savings | n/a | $19,000/mo |

That's roughly 70% of repeatable phone calls (order status, returns, the same five questions over and over) going to the AI, with the other 30% landing in front of your team in Gorgias. It's the same idea behind scaling customer service without hiring: move the routine volume to the AI and keep the headcount for the calls that need judgment. If you want round-the-clock coverage specifically, that's the case for 24/7 ecommerce phone support.

"My customers also feel like it's a normal person. They feel like they can communicate if they have questions."

Claudia Droge, TechCraft Studio

If your phone goes to voicemail after 6 p.m., book a 30-min call and we'll review your missed calls live. You'll see the phone-channel gap in your own numbers, not a slide.

Frequently asked questions

What is Gorgias's ARR in 2025? Gorgias has not published an official 2025 ARR. Its last well-sourced figure is roughly $69M ARR exiting 2024 (Sacra). At its 30%-plus growth rate, a directional 2025 estimate is the high-$70Ms to around $85-90M run-rate, but treat that as an estimate, not a disclosure.

How much revenue does Gorgias make? The two main public estimates for 2024 are $69M ARR (Sacra) and $72.6M revenue (Getlatka). Both land in the high-$60Ms to low-$70Ms. Gorgias is private and doesn't confirm exact figures.

What is Gorgias worth? Gorgias was valued at $530M in its May 2024 Series C, roughly an 8.8x forward revenue multiple at the time. The company has raised around $104M across 9 rounds, with Shopify, Sapphire Ventures, and Flex Capital among its investors.

How many customers does Gorgias have? Gorgias serves 15,000-plus ecommerce merchants worldwide, including about 40% of Shopify's top 1,500 brands. It's the top-rated customer service app on the Shopify App Store.

Is Gorgias profitable? Gorgias hasn't disclosed profitability. As a venture-backed SaaS company still growing 30%-plus and re-investing in AI, it's reasonable to assume it's prioritizing growth over reported profit, which is normal at this stage.

Does Gorgias do phone support? Gorgias is built for chat, email, and ticketing. Phone is not where it leads, which is why many brands run an AI phone agent like Ringly in front of Gorgias to handle inbound calls and escalate the hard ones into the helpdesk.

Talk to us

If you run a $10M-$100M Shopify brand on Gorgias and your phone still goes to voicemail after hours, a 30-min call is the fastest way to see what you're leaving on the table. We'll pull your missed calls and do the math live.

The 3-layer guarantee.

- Live in 14 days or it's free until launched.

- 65% resolution in 90 days or we refund the last 3 months of subscription fees.

- We keep working free until we hit 65%.

Ruben (Ringly co-founder) takes these calls personally.